The two major political parties are in a contentious battle over the Affordable Care Act (ACA). Republicans would like to repeal and replace it. Democrats are doggedly defending it.

But even if the ACA stays in place, there will still be almost 30 million people without health insurance and another 20 million or so who all too often face deductibles that are unreasonably high for moderate-income families and provider networks that are much too narrow for people with serious medical problems. If some Republicans get their way, things may not be much better. In fact, several Republican replacement plans are expected to insure even fewer people than under the current system.

We believe the health care system is desperately in need of reform. But the focus of that reform should not be the Affordable Care Act. The initial goal should be: making sure everyone has access to health insurance that is affordable and that gives them dependable access to medical care. Further, we believe that goal can be accomplished with money already in the system. We don’t need any new taxes or any new spending programs.

Most of the recommendations that follow are incorporated in bicameral legislation introduced in the House and the Senate by Pete Sessions and Bill Cassidy and in the Patient Freedom Act, sponsored by Senator Cassidy.

Remove The Perverse Incentives From The Individual Market

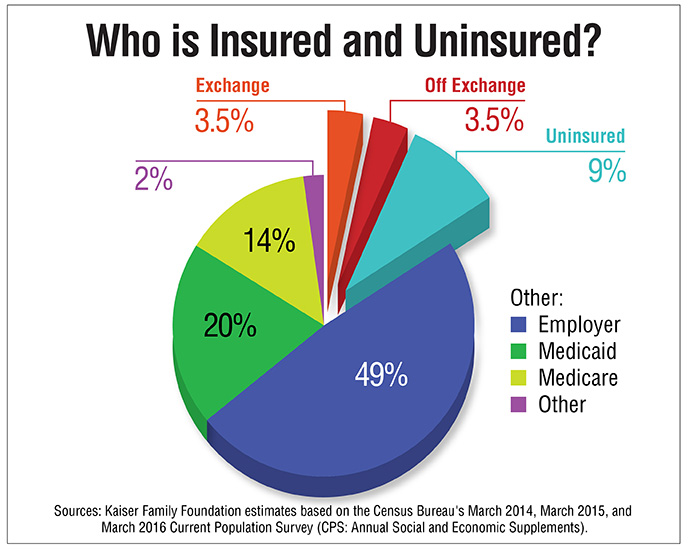

Figure 1 shows that there are currently about 21 million people obtaining health insurance in the individual market. About half are buying in the (Obamacare) exchanges and the rest are buying outside the exchanges.

Unwise public policies have allowed this market to become a dumping ground for people who are older and sicker than average. The states were allowed to end their high-risk pools and send their enrollees to the exchanges. The federal government did the same thing with the (Obamacare) risk pool (the Pre-Existing Condition Insurance Plan). Cities and counties are ending their post-retirement health care programs (which are almost always unfunded) and sending people to the exchanges, where they pay premiums that are well below the cost of their care thanks to limited age rating. That includes, for example, 8,000 former employees of the city of Detroit.

As premiums rise to meet the higher costs of the enrollees (they have roughly doubled in the past four years, on the average), healthier people are choosing to remain on the sidelines. Within the market, too many health plans are trying to survive by dumping their sickest, most costly enrollees on other plans—as they strive to attract the healthy and avoid the sick. Often they do this by offering narrow networks that omit the best doctors and the best hospitals and by saddling enrollees with high out-of-pocket costs. But, like a game of musical chairs, the sick don’t vanish—they simply move from plan to plan. In some states, the entire market is clearly in danger of entering a death spiral.

Neither Republicans nor Democrats have been willing to face up to an obvious fact: We have to stop this destructive behavior. We don’t have all the answers, but we believe part of the answer is “health status risk adjustment,” under which plans that send high-cost enrollees to other plans must top up the new premium to an actuarially fair level. This type of risk adjustment is designed to protect enrollees, unlike the current risk adjustment, which is designed to protect health plans instead. Only then will health plans seek to enroll the most costly patients instead of competing to avoid them. John Goodman and John Cochrane, in separate publications, have provided general outlines of how free market risk adjustment could work.

We cannot allow individuals to game the system by remaining uninsured while healthy and then enrolling after they get sick. The Medicare program seems to have solved this problem for Parts B and D and Medigap insurance—and it does so without any individual mandate. Medicare prevents adverse selection by penalizing people with higher premiums if they do not enroll when they are first eligible. Why not do what Medicare does?

Our legislation gives the states a great deal of discretion about how to deal with these problems. If they like the way their exchange is working they can keep it. But if they don’t like it, they are free to make radical changes.

Figure 1

Offer A Uniform Tax Credit To People Who Buy Their Own Health Insurance

The process of making the individual market functional may take a long time. While that is happening, we need to immediately change the way the federal government is subsidizing the insurance and the types of products insurers can offer. There should be one tax credit for the purchase of private health insurance. That credit may vary by age and geography, but it should be independent of income. Also, in every market there should be at least one plan available for the price of the credit, without any additional premium.

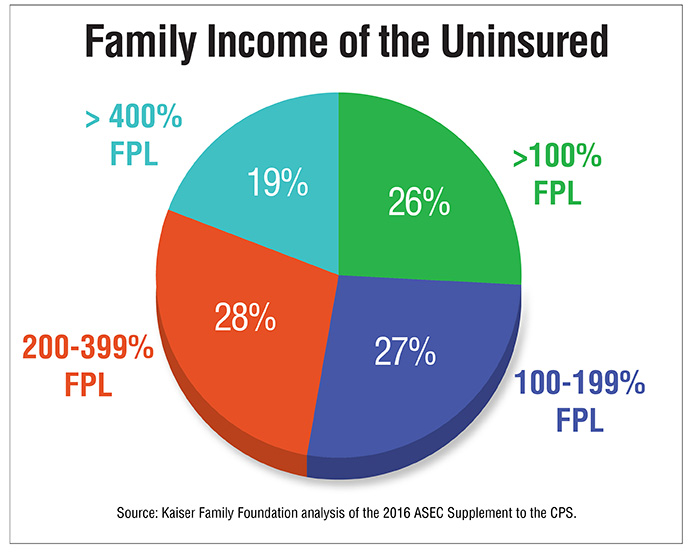

Figure 2 shows that a large number of the uninsured have low incomes. Many live paycheck to paycheck. If they have to pay any premium at all, millions of healthy people will decline the offer. If there is an income or asset test, enrollment becomes burdensome and complicated. With a uniform credit, states would find that streamlined, automatic enrollment is relatively easy.

How generous should the credit be? Right now, no one knows. In our legislation, we chose a number for 2017 that we think will allow the average person access to a health plan that is similar to well-managed, privately administered Medicaid. Ideally, plans would complete to see how attractive they can make their offer for that price. If, over time, we judge the minimum benefit package to be too skimpy, we can raise the amount of the credit. If we judge the amount excessive, we could lower it.

But right now, the market in many states is dysfunctional—in part because we have so completely suppressed and distorted normal economic incentives. That means competitive outcomes in many states can’t serve as a reliable guide to public policy decisions.

That’s why we need the next reform.

Figure 2

Offer The Same Tax Credit For Group Insurance

While we are trying to rescue the individual market—especially in places where it is most imperiled—people need a refuge from it. In general, the alternative to individual insurance is group insurance and in a great many cases group insurance is less costly and more generous than what is being offered on the individual market.

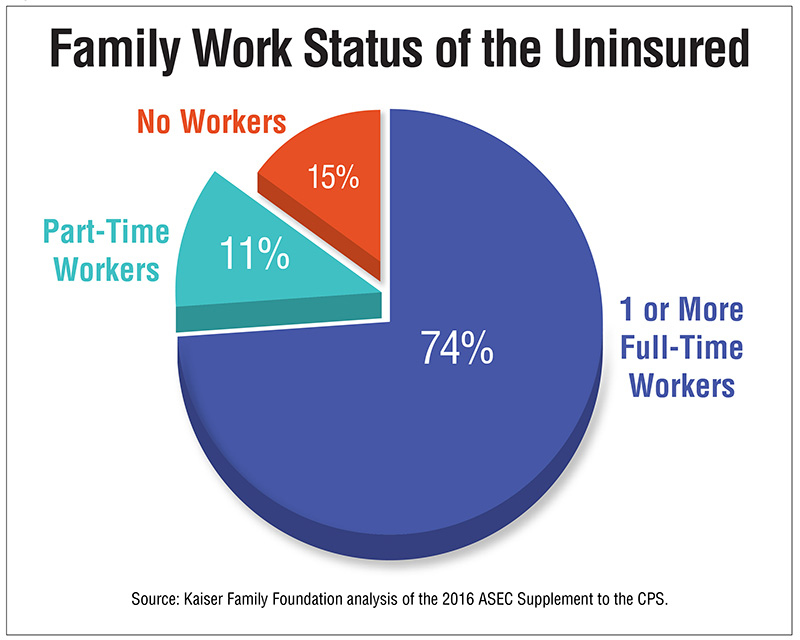

Under current law, employer-paid health insurance is excluded from the taxable income of the employees. For highly paid workers in Silicon Valley this is a generous provision—a subsidy that is worth more than half the cost of their health insurance. But for the low-wage employees depicted in Figure 3, the only tax that is being avoided is the 15.3 percent payroll tax.

One way to help bring stability to the individual market is to have it compete on a level playing field with the group market. In order for that to happen, employers need the option to take advantage of the same tax credit that is available in the individual market.

Let Employers Choose Between The Individual And Group Markets

Virtually all new government spending for private health insurance under the Affordable Care Act is going to what has become the most dysfunctional part of the health care system—the individual market. Almost every Republican plan to replace Obamacare makes the same mistake. But why throw good money after bad?

Figure 3 shows that 85 percent of uninsured live in a household with someone in the labor market. Like the Obamacare tax credit, our tax credit is refundable (you get it even if you don’t owe any taxes), advanceable (you don’t have to wait until next April to get it) and transferable (the money and the paper work can be transferred to an insurance company or—in our proposal—to an employer). If they are willing, it would be very easy for employers to use the credit to help employees enroll in a group plan that could give them access to lower premiums and better coverage.

Figure 3

Let Employers Choose The Employee’s Tax Benefit

One reason why so little progress has been made in increasing the number of people with employer-based insurance is that larger employers are meeting the Affordable Care Act’s mandate by offering their low-wage employees Bronze plans with deductibles of $6,000 or more and asking for premiums equal to 9.5 percent of the employee’s wage. Plus, employees have to pay the full premium for their dependents. These plans are great for hospitals who occasionally encounter a million-dollar pre-mature baby, but they leave families exposed to pay out of pocket for 95 percent of all likely medical encounters. No wonder employees routinely reject these offers. And when they reject them, they are not entitled to subsidized insurance (except in a few rare circumstances) in the exchanges and they are subject to fines each year.

As an alternative, we propose to get rid of the employer mandate and give employers a choice of buying insurance for their employees in the individual or the group market. We also propose to give employers a choice of tax regimes: a tax credit or a tax exclusion.

Let Employers Offer Their Employees Personal And Portable Insurance

Public opinion polls have consistently shown that what employees most want in health insurance is portability. They want to be able to take their insurance with them from job to job. Many employers would like to accommodate that preference by giving each employee a “defined contribution” and letting them choose their own health insurance. Health Reimbursement Arrangements (HRAs) are ideally designed to accommodate this practice.

Also, where the individual market is working, portable insurance reduces the likelihood of uninsurance after a job change, reduces the problems of pre-existing conditions, and enhances the likelihood that patients will receive continuity of care.

For those reasons, allowing use of pre-tax dollars to help employees purchase health insurance should be extended to all employers. Lest you think this is pie-in-the sky wishful thinking, Congress just did something similar for small business.

The 21st Century CURES Act, which recently passed both houses of Congress with large bipartisan majorities, created a special opportunity for employers with fewer than 50 workers. Small employers can (1) pay taxable wages and allow their employees to buy their own insurance—benefiting from the Obamacare tax credits if they qualify; or (2) pay less in wages and use pre-tax dollars to provide health insurance directly; or (3) use HRAs to help employees buy their own health insurance with pre-tax dollars

[Note: employees cannot double dip—either they get the tax benefit from pre-tax purchase or they get a tax credit, but not both.] This represents an abrupt policy reversal for the Obama administration, which has been threatening to fine any employer who uses HRA accounts in this way as much as $100 per employee per day. This is the largest fine for any offense related to the ACA.

There is one option we would like to add to this list: As explained above, small employers should be able to buy group insurance with employee tax credits as opposed to buying that insurance with pre-tax dollars. Then, we would like to extend all of these choices to every employer.

That would leave us with a system in which employers would have complete freedom of choice between the individual and group markets and complete freedom of choice of how their employees will receive tax relief.

Integrate Medicaid And Private Insurance

Between 100 percent and 200 percent of the federal poverty level, families typically become eligible and ineligible for Medicaid many times over the course of several years. About 29 million people will shift eligibility between Medicaid and subsidized exchange insurance in a single year. Only one in five adults on Medicaid remain continuously eligible over a period of four years. This churning is not just administratively inconvenient. It is expensive. Lack of continuity of care also affects health.

As an alternative, we propose to allow families to be able to leave Medicaid, claim the tax credit, and enroll in private insurance instead. They could remain there, regardless of how their income changes. Also, two-thirds of Medicaid enrollees nationwide are currently in private sector plans that contract with state Medicaid programs. These contractors should be able to offer the same plan in the individual market, so that people could remain in that plan as their income (and therefore their eligibility for Medicaid) changes.

As incomes rise and fall, the help families get from the government may change; but they would not have to change health plans.

Create An Effective Safety Net

The ultimate goal of health reform is access to health care. Health insurance is merely a means to that end. No matter what we do, there will always be some people who are uninsured. Ours is the first legislation ever introduced that has a mechanism to integrate tax subsidies for private health insurance with assistance for the health care safety net.

For people who are not on Medicaid or other public insurance and who do not have private insurance, a portion of unclaimed tax credits would be returned to communities where the uninsured live. Money follows people. If the number of uninsured rises, safety-net hospitals would get more funds. If the number falls, federal dollars would shift to support private health insurance.

Under the proposals outlined above, there is no reason for anyone to be uninsured. We will have achieved a goal the sponsors of the Affordable Care Act promised to reach, but never delivered. And in case some fall through the cracks and remain uninsured, an adequately funded safety net will insure access to medical care.