The Fed met market expectations by cutting its target for the fed funds rate by 25 basis points, down to the range of 1.75 - 2.00 percent. In this post I want to demonstrate just how boxed in the Fed has now become, with the help of 3 charts.

First, let’s review just how low interest rates have been (and still are), in a long-term historical context:

As the chart shows, the (effective) fed funds rate was in this range back during the early 2000s, which helped spawn the housing bubble and bust (as I predicted in this Mises.org article which ran 11 months before the financial crisis). Before then, we have to go all the way back to the early 1960s to see rates this low. And furthermore, to the extent that Mises was right, and artificially low interest rates lead to an unsustainable boom, then the seven years of virtually zero percent interest rates (from December 2008 - December 2015) have fostered a plethora of malinvestments.

Now here’s the irony: In the midst of the Fed cutting rates, and injecting $75 billion in repo operations on Tuesday to push down a spike in short-term rates, at least on paper we see that everything seems to be fine. Specifically, consumer price inflation is a bit lower than the Fed’s desired level but is still at a “healthy” 1.8% (year over year, as of August), while the official unemployment rate is still at a 50-year low:

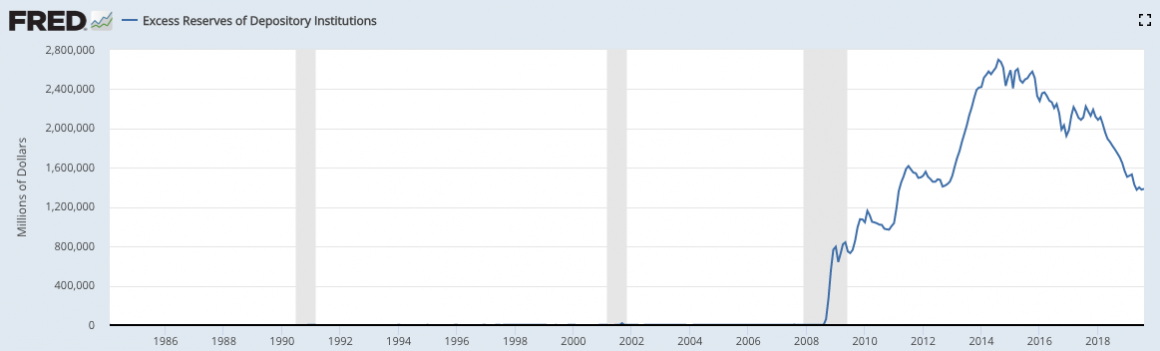

Finally, despite the apparently healthy economy (vis-a-vis the Fed’s “dual mandate”), there is still an extraordinary stockpile of excess reserves in the banking system, relative to the pre-crisis era:

Medical metaphors for economics are never perfect, but we can certainly say this: Far from being in the midst of a robust “recovery,” the patient—i.e. the US economy—is still incredibly weak, needing constant infusions of medicine to stave off a crisis in its circulation.

On the one hand, it’s refreshing that Fed officials don’t think the economy can be summed up in two numbers, namely the official unemployment and consumer price inflation rates. But on the other hand, the fact that the Fed is cutting rates now, in spite of the “healthy numbers,” is an ominous indication of just how deep the rot goes in the economy’s capital structure.

Unfortunately, the world may soon see exactly why 7 years of unprecedently loose monetary policy was a very foolish idea.